What it is

What is a Transition to Retirement Pension?

Our Transition to Retirement Pension is an account which allows you access to your super as an income stream while you are still working. This could suit you should you choose to reduce your work hours, as the income you receive from your super benefits can help to make up for any loss of salary you may have.

If you still want to work the same hours, you may consider using a Transition to Retirement Pension as a way to increase your income, or to maximise your retirement savings through salary sacrifice. There may be some tax benefits for you, however we recommend that you seek personal financial advice before making a decision.

To be eligible to open a Transition to Retirement Pension, you must have reached your Commonwealth preservation age (shown below).

A Transition to Retirement Pension does not allow lump-sum cash withdrawals, so it is also known as a non-commutable income stream. However, once you retire, you’ll be able to review your options and consider setting up a regular RI Allocated Pension.

Is transition to retirement right for you?

Transition to retirement is a way you can access your super while you’re still working.

Take our simple quiz to see whether it could be right for you.

The benefits of a Transition to Retirement Pension

With a transition to retirement strategy in place, you could:

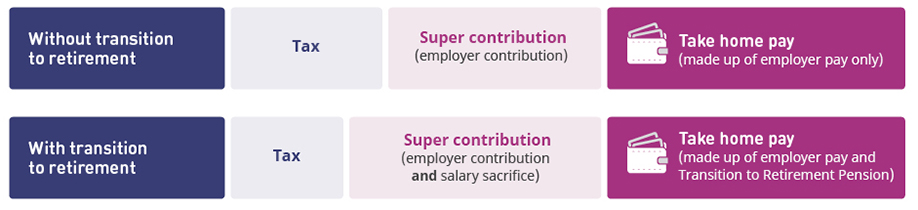

- Increase your super - you'll continue to work and can sacrifice some of your salary to super

- Reduce your hours - you can work less without reducing your overall income, as your pension can make up for your lower salary

- Increase your income - you'll be receiving an income stream from a pension as well as your normal salary

You can find the right balance to suit your needs, with the flexibility to change your strategy as your circumstances change. We recommend that you speak with a financial adviser, accountant or tax adviser to help you decide if our Transition to Retirement Pension is right for you.

There are a number of ways you can use transition to retirement to benefit you:

- Transition to retirement with GESB Super

- Transition to retirement with West State Super

- Transition to retirement with Gold State Super

What is your Commonwealth preservation age?

To be eligible to open a Transition to Retirement Pension from your GESB Super or West State Super account, you need to have reached what’s known as your preservation age:

Your preservation age depends on your date of birth. The preservation age increased to 60 for those born after 30 June 1964. As of 1 July 2024, if you are aged 60 or more, you have reached your preservation age.

If you’re a Gold State Super member, you can start a Transition to Retirement Pension from the age of 55 but you’ll pay more tax if you access your super before you reach the Commonwealth preservation age.

Transfer balance cap

It is important to note that the transfer balance cap of $2.1 million does not apply to transition to retirement income pensions. Find out more about the transfer balance cap.

Thank you for printing this page. Remember to come back to gesb.wa.gov.au for the latest information as our content is updated regularly. This information is correct as at 02 August 2026.