Statement of Corporate Intent 2026/27

June 2026

1. Introduction

This is the Government Employees Superannuation Board’s (GESB’s) Statement of Corporate Intent for the 2026/27 financial year. It includes an overview of GESB, our operating environment, strategic focus areas, performance targets and financial forecasts for 2026/27.

As at 31 December 2025, GESB had funds under management (FUM) of $46.7 billion (bn) with more than 278,000 member accounts for more than 250,000 current and former Western Australian (WA) public sector workers.

The superannuation industry continues to operate in a climate of change with ongoing mergers, increasing competitive intensity, strong focus on retirement outcomes for members, rapid technological change, increasing member expectations, and continuing reforms from the Australian Government.

Within this changing environment, we remain committed to providing high quality, value for money products and services that meet our members’ needs. We aim to help members achieve a quality retirement and be the fund of choice for current and former WA public sector employees. This is achieved by providing competitive long-term investment returns and low fees for members, ensuring we are well positioned in comparison to the leading Australian superannuation funds, and attracting and retaining high quality people.

Being based in WA provides us with a unique opportunity to provide easy access for our members and insurance tailored to WA public sector employees. We pride ourselves on providing member-first services, being secure and trustworthy and on having a high level of engagement with employers.

We have a unique opportunity and competitive advantage in the personal service we provide when members engage with us to make decisions regarding their superannuation and retirement. We also aim to meet member expectations with respect to digital engagement and invest in experience improvements that provide value.

We have four strategic objectives:

- Strong financial outcomes for members

- Positive member experience

- Efficient and effective operations

- Positive culture and stakeholders

In response to our operating environment and member expectations, we have three strategic focus areas (SFAs):

- Our Retirement Income Strategy

- Our Member Support Strategy

- Enhancing our foundations to uplift our culture, capability and technology to set GESB up for the future changing environment

Each SFA is supported by key projects, operational priorities, and business as usual activity to achieve one or more of our four strategic objectives.

2. GESB profile

For more than 85 years, GESB has been the default fund for most of the WA public sector and has helped members achieve a quality retirement by looking after their superannuation, providing insurance they can rely on, and delivering an exceptional member experience.

Our purpose | To help members achieve a quality retirement |

|---|---|

Our vision | To be the fund of choice for current and former WA public sector employees |

Our mission | To responsibly manage members’ retirement savings, achieve long-term investment objectives and provide relevant support so members can make informed decisions |

| Our strategic objectives |

|

| Our values | Put members first Sustainable performance Achieve together Act with integrity |

| Our value proposition |

|

3. Operating environment

3.1. Regulatory and governance environment

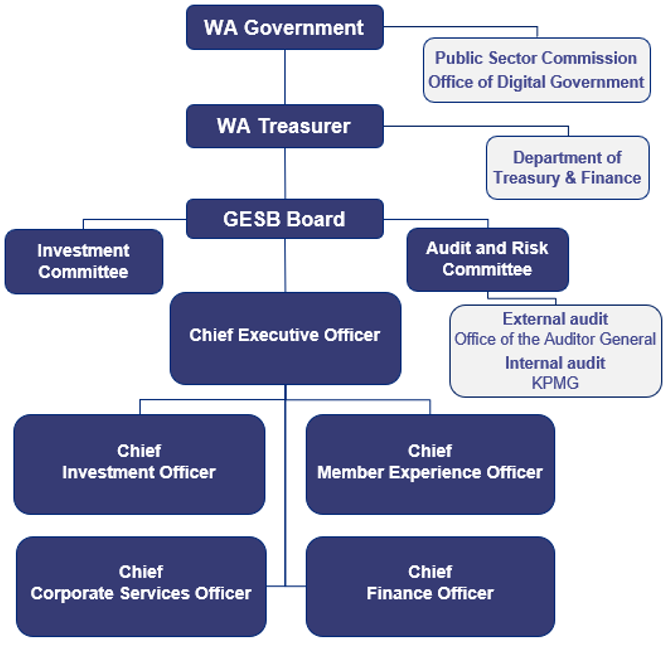

GESB is a statutory authority, responsible for administering the superannuation schemes established and continued under the State Superannuation Act 2000 (SSA), in addition to other defined benefit schemes on behalf of the State. The responsible Minister for GESB is the Treasurer of Western Australia (the Treasurer).

GESB’s statutory and regulatory framework is principally derived from:

- The SSA and the State Superannuation Regulations 2001 (SSR)

- Treasurer’s Guidelines issued pursuant to the SSA

- The Heads of Government Agreement (HoGA) between the State and the Australian Government

The superannuation schemes administered by GESB are Exempt Public Sector Superannuation Schemes (EPSSS). EPSSSs are deemed to be complying superannuation funds for the purposes of Australian Government superannuation and taxation legislation. However, the schemes are not subject to the Superannuation Industry (Supervision) Act 1993 (SIS Act), nor is GESB subject to Australian Prudential Regulation Authority (APRA) supervision.

GESB also administers the Parliamentary Pension Scheme and Judges Pension Scheme on behalf of the Parliamentary Superannuation Board and the Treasurer respectively. These schemes are not included in the GES Fund.

Governance and management structure

3.2. Legislation/policy changes

Our purpose, vision, mission and strategic objectives are determined within the context of our enabling legislation and the HoGA between the State of WA and the Australian Government. They reflect State and Australian Government policy objectives and GESB’s statutory obligation to act, as far as practicable, in the best interests of members.

State

Our strategy is aligned with the WA Government’s Outcomes Based Management framework and priorities.1

Australian Government

GESB is not APRA regulated, however, under the HoGA, the State of WA has committed to conform with the principles of the Australian Government’s retirement income policy to the best of its endeavours. Therefore, we review all Australian Government reforms and the prudential standards applicable to APRA regulated funds to determine how GESB can align with them as far as is practicable.

Relevant current retirement income reforms and policy include:

- The Treasury Laws Amendment (Your Future, Your Super) Act 2021

- Retirement Income Covenant introduced to the SIS Act (2022)

- Improving the Retirement Phase of Superannuation (2024) including consultation papers: ‘Best practice principles for superannuation retirement income solutions’ and ‘The retirement reporting framework’ (2025)

- Treasury Law Amendments (Payday Superannuation) Act (2025) and Superannuation Guarantee Charge Amendment Act (2025)

- Prudential Standard SPS515 Strategic Planning and Member Outcomes (effective 1 July 2025) and CPS 190 Recovery and Exit Planning (2025)

- Treasury Laws Amendment (Delivering Better Financial Outcomes and Other Measures) Act 2024 (Tranche 1) and Draft Tranche 2

- The Treasury Laws Amendment (Supporting Choice in Superannuation and Other Measures) Bill (2025)

- Mandatory and enforceable service standards for the superannuation industry (consultation 2025 and projected start date July 2028)

- Treasury Law Amendment (Building a Stronger and Fairer Superannuation System Act

3.3 The superannuation environment

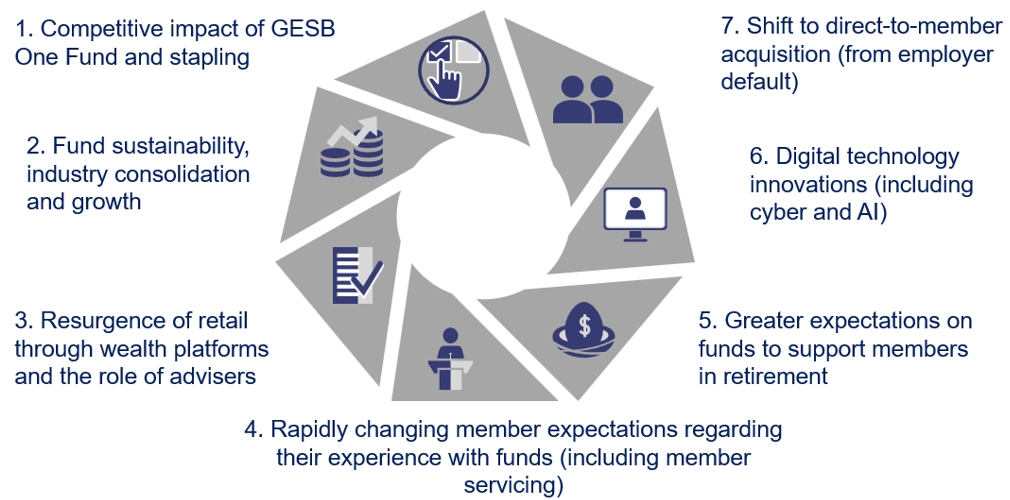

The Australian superannuation industry is worth over $4.5 trillion (30 September 2025) and the environment continues to evolve at a rapid pace with the following trends:

- Increasing competitive intensity as the industry focuses on attracting new and retaining existing members

- Focus on retirement outcomes as a large proportion of the Australian workforce becomes eligible to drawdown their superannuation

- Rapid technology change and ability to provide services at scale

- Increased cyber threats as criminals seek to obtain funds from an industry growing faster than the Australian banking system

- Continuing regulatory reforms and expectations driven by the Australian Government and regulators

- Rising member expectations

- Changes to the investment landscape including funds:

- Leveraging their size to access global-scale investment opportunities and improve operational efficiency

- Focusing on impact investing through ESG and net zero targets expected by members and broader stakeholder groups

- Changing their investment approach to utilise passive investment options, increase investment in private markets as well as digital infrastructure and renewable energy in response to the rise of AI creating a demand for power

- Ongoing merger activity as funds seek to gain scale to meet members’ best interests

In this environment the trends that impact GESB’s strategy are:

4. GESB's strategy

4.1. Strategic objectives

| Strategic objectives | Objectives |

|---|---|

| 1. Strong financial outcomes for members | 1.1 Returns meet long-term objectives and are competitive against other comparable superannuation funds 1.2 Fees in the lowest quartile of APRA funds 1.3 Insurance cover does not inappropriately erode superannuation balances |

| 2. Positive member experience | 2.1 Members have a high level of satisfaction with their interactions and communication with GESB 2.2 Members have access to quality products and services that support them in accumulation and retirement 2.3 Members in pre-retirement and retirement feel confident in their retirement planning and can make informed choices |

| 3. Efficient and effective operations | 3.1 Maintain sufficient scale and fund sustainability 3.2 Efficient and effective delivery of services and operations 3.3 Strong governance, risk and compliance framework |

| 4. Positive culture and stakeholders | 4.1 High performing culture and capable, knowledgeable and engaged staff 4.2 Highly regarded by stakeholders |

4.2. Strategic focus areas

Based on our value proposition, we have a unique opportunity and competitive advantage in the personal service we provide when members engage with us to make decisions regarding their superannuation and retirement. We also aim to meet member expectations with respect to digital engagement and invest in experience improvements that provide value.

To deliver our strategic objectives and respond to legislative change and trends in our operating environment, we have identified three strategic focus areas (SFAs).

| SFA | Description |

|---|---|

| Retirement Income Strategy | Our Retirement Income Strategy supports members who are retired or are approaching retirement to plan and achieve a quality retirement, aligned to the objectives of maximising retirement income, managing risks and providing flexible access to funds over the period of retirement. It focuses on better understanding our members’ needs, enhancing our retirement products and broadening the help, guidance and support we provide so they can make informed decisions about their superannuation and retirement |

| Member Support Strategy | Our Member Support Strategy comprises investment in initiatives that guide how we interact with members, ensuring consistent, high-quality support across all touchpoints. It focuses on omnichannel support and proactive engagement, using technology (e.g. digital learning hub and calculators), and continuous improvement through feedback and performance metrics to help members achieve a quality retirement |

| Strategic Enablers | Investment required in culture, capability, and digital and technology to strengthen our ability to deliver value to our members in the long-term in line with their needs and our aspirations to better support members |

4.3. 2026/27 work programs and projects

In our planning for 2026/27, we have grouped projects into five programs of work aligned to achieving our objectives and delivering our SFAs.

| Program | Description |

|---|---|

| Technology and Digital Uplift | Aligned with our integrated technology and digital strategy, our focus is on delivery of digital and technical solutions that improve operational efficiency, strengthen cyber protection, enhance self-service, provide real-time information and improve the overall online experience for members |

| Enhanced Communications and Interactions | Enhancing delivery of data-driven, personalised, proactive engagement across various member cohorts, and appropriate information and education materials that support members in all aspects of decision making |

| Enhanced Products and Services | Ensuring our products and services meet member needs, in particular reviewing our current retirement product and advice offerings and providing the range of services (online, phone and face-to-face) that supports members in achieving their retirement outcomes |

| Fund Sustainability | For GESB to remain sustainable and continue to deliver outcomes to members, we focus on managing operating costs and on initiatives that lead to acquisition and retention of members in the face of competition, particularly through advisers and platforms, and the introduction of stapling for public sector employers |

| High Performing Culture | Having a high-performing culture is critical for achievement of our strategic objectives and our focus is on building receptiveness to change, innovation, effective risk management, wellbeing, and communication |

2026/27 projects and initiatives

Enhanced communications and interactions

| Initiative | Description | Strategic focus areas |

|---|---|---|

| Member online enhancements - pension page | Uplift RI-AP members' ability to manage (self-serve) their accounts online, including pension payments and commutations |

|

| Digital member identification | Uplift member identity verification for enhanced security, high accuracy, and enhanced user convenience to remain at the forefront of the industry |

|

| Personalised member experience | Delivery of personalised experiences through the uplift and use of member data and development of psychographic personas |

|

| Enhanced omni-channel experience | Enhanced member-centric experience with integrated touchpoints and channels |

|

| Enhanced voice of customer program | Enhance GESB's voice of member and employer programs to uplift the timeliness of gathering, analysing, and acting on member, employer and adviser feedback |

|

Technology and digital uplift

| Initiative | Description | Strategic focus areas |

|---|---|---|

| GESB Enterprise Integration Layer (EIL) | Progress development of a foundational middleware (EIL) to connect systems, streamline data flow and automate processes |

|

| Review digital member asset arrangements | Review digital member asset arrangements including architecture for GESB's website, Member Online and member app (aligned to GESB's digital and technology strategy and roadmap) to support uplift of member experience and efficient servicing |

|

| GESB digital member mobile application | Tender and commence implementation of a mobile app for members |

|

Enhanced products and services

| Initiative | Description | Strategic focus areas |

|---|---|---|

| AIA Vitality member program | Pilot AIA Vitality - a personalised, science-backed program that supports the health and wellbeing of members |

|

| Fortnightly pension payments | Enhance our RI-AP product by offering fortnightly pension payments |

|

| GSS unclaimed money | Inclusion of the Gold State Super (GSS) scheme in the ATO unclaimed money regime |

|

| GESB provision of financial advice | Finalise development of financial advice roadmap including expansion of our retirement options service |

|

| Default retirement option and longevity options | Review provision of (and implement where relevant) Managed Default and/or longevity options for retired members |

|

| GSS portability | Implement portability of GSS benefits for deferred members under age 55 |

|

| Adviser servicing and engagement program | Implement program to support advisers in the provision of appropriate advice and service to our members |

|

| Digital adviser portal | Build portal to allow advisers to self-service information for their GESB member clients |

|

Fund sustainability

| Initiative | Description | Strategic focus areas |

|---|---|---|

| Public sector onboarding & employer stapling | Procure and implement employee onboarding solutions for WA public sector employers and support them in implementation of stapling |

|

| Repricing implementation | Review GESB pricing |

|

| Insurance rate guarantee | Commence work to assess AIA claims experience and product offering in preparation for end of rate guarantee |

|

| Enterprise Resource Planning (ERP) | Commence implementation of ERP application |

|

| Cheque elimination | Program to remove use of cheques as Commonwealth government cheque transition plan aims to remove issuance of cheques by 30 June 2028 and acceptance of cheques by 30 September 2029 |

|

| AI - implementation of use cases (internal) | Implement use cases of generative AI to deliver operational efficiencies |

|

| Cyber security maturity enhancement | Enhancement of our systems and processes to manage cyber related risks | |

| GRC system procurement | Market testing and procurement process for governance, compliance and risk system |

|

High performing culture

| Initiative | Description | Strategic focus areas |

|---|---|---|

| GESB office move | Relocation to fit for purpose office premises | |

| Capability framework (including leadership) implementation | Implement expanded professional development and performance management programs, including wellbeing and leadership capability frameworks |

|

4.4. Operational priorities and initiatives

In addition to the SFAs, we continue to focus on our operational priorities and continuous improvement to meet our objectives.

Strategic objective 1: Strong financial outcomes for members

1.1 Returns meet long-term objectives and are competitive against other comparable superannuation funds

- Annual investment ‘health check’ review of Strategic Asset Allocation and investment objectives and regular program of investment asset class reviews

- Review of Treasurer’s Prudential Guidelines for Investments to support better practice investment governance

- Maintain a comprehensive performance monitoring and reporting regime to assess the extent to which the Board’s investment objectives are being achieved, including performance against comparable superannuation funds

1.2 Fees are in the lowest quartile of APRA funds

- Annual scheme pricing review to ensure GESB fees remain well positioned against peers

- Comprehensive review of our Reserving Strategy

1.3 Insurance cover that does not inappropriately erode their superannuation balances

- Providing appropriate insurance cover with suitable pricing that does not inappropriately erode members’ superannuation balances, including assessing claims experience and product offering in preparation for end of rate guarantee

Strategic objective 2: Positive member experience

2.1 Members have a high level of satisfaction with their interactions and communication with GESB

- Member engagement initiatives that provide consistent high-quality support across all touch points

- Using member journey mapping to develop key encounters and pinpoint where help matters most for different personas

- Ongoing enhancements to member service and engagement through our Member Services Centre, Insurance Claims Consultants, live online chat, Retirement Options Service, seminars and webinars

- Continuous improvement of digital tools, services, content and engagement channels

- Reviewing member feedback and complaints to ensure appropriate outcomes and identify process or product improvements

- Continued focus on improving support and services for members when they are in a vulnerable position and ensuring our information and content is accessible to all members

- Further progressing our Reconciliation Action Plan to create tangible outcomes for Aboriginal and Torres Strait Islander stakeholders in our workplace, membership and community

2.2 Members have access to quality products and services that support them in accumulation and retirement

- Regular assessment of product and service settings, and business performance, to remain competitive and support member outcomes

- Providing appropriate insurance cover with flexible, easy to use, value-for-money insurance products that members can rely on including implementing digital enhancements to insurance underwriting processes

- Working closely with MUFG (fund administrator) and AIA Australia (group insurance provider) to ensure that insurance claims are processed in a timely, efficient and respectful manner, with appropriate outcomes

2.3 Members in pre-retirement and retirement feel confident in their retirement planning and can make informed choices

- Ongoing implementation of initiatives that support members who are retiring or in retirement to make informed choices. This includes provision of Retirement Options Service and advice services, seminars and webinars, progressively building a self-service learning hub with online information and tools (e.g. additional calculators) and partnering with other agencies for retirement-related support

Strategic objective 3: Efficient and effective operations

3.1 Maintain sufficient scale and fund sustainability

- Ensuring robust governance, oversight and management of material outsourced providers: MUFG, Frontier Advisers Pty Ltd (asset consultant), Northern Trust (global custody services), Squiz (member digital services) and AIA Australia

- Continued management of costs to provide value for money products and services to our members

3.2 Efficient and effective delivery of services and operations

- Working closely with MUFG to continuously improve our service delivery and uplift service standards to meet rising member expectations, and ensure our services are competitive across the superannuation industry

- Supporting employers with Payday superannuation compliance

- Exploring opportunities to deliver operational efficiencies, including potential uses of AI and implementing high-value AI use cases

3.3 Ensuring we have a strong governance, risk and compliance framework

- Maintaining a strong governance, risk and compliance framework to facilitate the effective and risk-managed operation of GESB within the requirements of governing legislation

- Enhancing our systems and processes to manage emerging cyber-related risks and evolving threats, particularly to ensure security of member information and maturing our control framework that aligns with the State’s cyber security policy

- Integrating prudent ESG management throughout our investment process and in our business operations

- Delivering to our ESG roadmap, aligned with our 2050 net zero carbon emissions commitment. This includes a 45% reduction in the carbon intensity of our listed equity portfolio (including listed property and listed infrastructure) by 2030, and net zero carbon emissions for our Unlisted Property portfolio by 2040 Strategic objective

Strategic objective 4: Positive culture and stakeholders

4.1 High performing culture and capable, knowledgeable and engaged staff

- Strengthening organisational capacity by preparing our people for the workforce of the future, including flexibility and productivity

- Development and rollout of professional development programs, wellbeing framework and leadership capability framework

- Improving our staff training and performance management frameworks

- Driving meaningful cultural change by proactively implementing solutions that address staff survey feedback

- Relocation to fit for purpose office premises

4.2 Highly regarded by key stakeholders

- Building on our strong relationships with key agencies, WA public sector employers and public sector unions

- Supporting public sector employers in meeting their superannuation obligations

- Extending the reach of our high-quality employer and member workplace information and education programs

5. Performance and risk management

5.1 Performance targets

Our strategic objectives reflect our focus of providing strong financial outcomes to members, competitive long-term investment returns that meet our objectives, low fees, and improved member engagement with their superannuation. We are also focused on providing ongoing assistance to employers to fulfil their superannuation obligations.

The performance measures in this report measure value provided to members and the quality of the services delivered. These include key effectiveness and efficiency performance indicators, as required by the Financial Management Act 2006.

Performance measures (2026/27) | |

|---|---|

Measures | Targets |

GSS returns v primary objectives | Achieve Average Weekly Earnings +2.5% p.a. over rolling five-year periods |

GESB Super default plan returns v primary objectives | CPI +3% p.a. over rolling seven-year periods |

WSS default plan returns v primary objectives | CPI +3% p.a. over rolling seven-year periods |

Retirement Income conservative plan returns v primary objectives | CPI +2% p.a. over rolling five-year periods |

GSS, GESB Super, WSS and RI Allocated Pension returns v secondary objectives | Exceed asset weighted benchmark return over rolling three-year periods |

Administration cost per accumulation account | $264 |

Administration cost per defined benefit account | $330 |

Member satisfaction with service | 80% |

Management expense ratio (MER) (excluding contribution to reserves) | 0.30% |

Other performance measures | |

|---|---|

Key performance measures | Targets |

GESB Super, WSS and Retirement Income fee quartiles | Bottom (lowest fee) quartile |

Employer satisfaction | 75% |

Funds under management | $49.4bn |

Net funds flow | $377m |

Administration expenses | $82.3m |

Cost to asset ratio | 0.2% |

Staff satisfaction | 70% |

Staff turnover | <10% |

5.2 Risk management

Our risk management strategy addresses risks that may adversely impact members, staff, assets, operations and our outsourced service providers. The strategy meets the requirements of subsection 52 (8) of the SIS Act, APRA Standards CPS220 and CPS230 and International Risk Management Standard ISO 31000.

The Executive Leadership team continues to provide robust oversight of the risk landscape, conducting quarterly reviews of material risks and mitigation progress. Findings are reported to both the Audit and Risk Committee and the Board.

The Board conducts an annual review of GESB’s material risks and approves the material risks for the coming financial year.

Fund unsustainability has been added as a material risk since the last review. Having a sustainable business model is important for us to continue to provide quality, value-for-money member outcomes over the long-term. It is a focus area for the superannuation industry, including APRA, which has an objective of financial system stability.

| Key material risks |

|---|

1. Failure to continue to deliver member outcomes and meet member expectations |

2. Failure to deliver investment returns that meet objectives |

3. Financial crimes against GESB and/or members |

4. Failure to achieve satisfactory outcomes in relation to material outsourced providers |

5. Material operational disruptive event |

6. Material cyber risk |

7. Deterioration in leadership, capacity, capability and/or culture |

8. Loss of external stakeholder trust |

9. Fund unsustainability |

6. Financial forecasts

For the Financial Year Ending 30th June | Projected Actual | Budget |

|---|---|---|

Opening Net Assets | 44,153,352 | 47,195,124 |

Income from Investments | 3,027,628 | 2,589,803 |

Superannuation Revenue | 6,198,990 | 6,151,699 |

Other Income | 7,544 | 8,574 |

Total Revenue | 9,234,162 | 8,750,076 |

Superannuation Benefit Payments | 5,463,836 | 5,774,512 |

Administration Expenses | 71,346 | 82,167 |

Investment Expenses | 136,061 | 144,551 |

Loan Interest | - | - |

Other Expenses (incl Tax) | 521,146 | 538,686 |

Total Expenses | 6,192,389 | 6,539,915 |

Closing Net Assets | 47,195,124 | 49,405,284 |

Net Assets by Scheme

For the Financial Year Ending 30th June | Projected Actual | Budget |

|---|---|---|

Defined Benefit Schemes (Gold State Super and Pension Scheme) | 3,289,656 | 2,920,288 |

West State Scheme | 22,656,865 | 22,739,401 |

GESB Super | 12,832,053 | 14,983,188 |

Retirement Income - Allocated Pension | 8,146,842 | 8,493,156 |

Retirement Income - Term Allocated Pension | 9,908 | 8,714 |

Reserves | 259,799 | 260,537 |

Total Assets | 47,195,124 | 49,405,284 |

Accumulation Scheme Surplus Deficit

For the Financial Year Ending 30th June | Projected Actual | Budget |

|---|---|---|

West State Super | 705 | (4,813) |

GESB Super | 7,982 | 8,280 |

Retirement Allocated Pension | (7,642) | (9,216) |

Retirement Term Allocated Pension | (1) | (8) |

Total Accumulation Scheme Surplus/(Deficit) | 1,044 | (5,757) |

Administration Expenses

For the Financial Year Ending 30th June | Projected Actual | Budget |

|---|---|---|

In house Administration Expenses | 11,704 | 17,457 |

Employment Expenses | 19,641 | 20,475 |

Outsourced Administration Expenses | 34,678 | 38,507 |

Total Administration Expenses | 66,023 | 76,439 |

Cost per Account

For the Financial Year Ending 30th June | Projected Actual | Budget |

|---|---|---|

Average cost per Accumulation Account | 230 | 264 |

Average cost per Defined Benefit Account | 258 | 330 |

Government Services Recoup

| Benefit Payments | Projected Actual | Budget |

|---|---|---|

Gold State Super | 230,292 | 209,583 |

Pension Scheme | 134,736 | 127,337 |

Parliamentary Pension Scheme | 10,959 | 11,250 |

Judges Pension Scheme | 24,217 | 25,028 |

Total Recoup of Benefit Payments | 400,204 | 373,198 |

| Administration Expenses | Projected Actual | Budget |

|---|---|---|

Gold State Super | 5,326 | 6,243 |

Pension Scheme | 1,134 | 1,139 |

Parliamentary Pension Scheme | 182 | 226 |

Judges Pension Scheme | 155 | 192 |

Government Services | 278 | 306 |

Total Recoup of Administration Expenses | 7,076 | 8,106 |

Total Consolidated Account Recoup | 407,280 | 381,304 |

Note: Projected actual as at 29 March 2026

Total FUM is projected to increase to $49.4 bn by June 2027. FUM is reported in the financial statements as investments plus cash and cash equivalents. GESB prepares its financial statements in accordance with Australian Accounting Standards, including AASB 1056 Superannuation Entities and other authoritative pronouncements of the AASB as applied by the Treasurer’s Instructions and the SSA.

1 Government of WA: Outcomes Based Management, Guidelines for use in the WA Public Sector, October 2025

Page last updated 17 June 2026Thank you for printing this page. Remember to come back to gesb.wa.gov.au for the latest information as our content is updated regularly. This information is correct as at 03 August 2026.